info@crma.com

1-919-973-9011

help@crma.com

ABOUT US

Company Overview

Executive Leadership

PRODUCTS

Allowance Leader (Comprehensive CECL Solution)

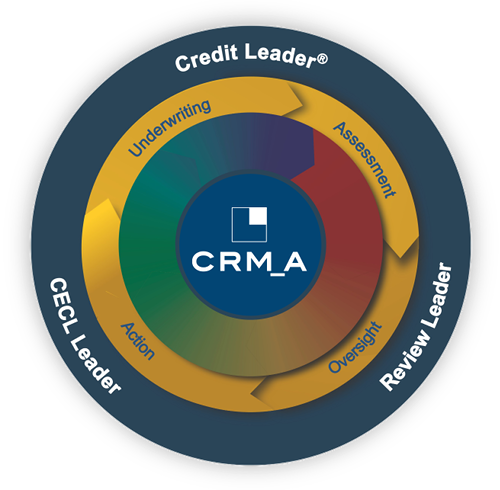

CRM_A Credit Leader

®

Underwriting, Risk Grading & Workflow Platform

CRM_A Online Credit Manual

CRM_A Toolbar

®

(Comprehensive Cash Flow Analysis)

Quantitative Products

Stress Testing

Loan Pricing

SERVICES

Loan Review & Due Diligence

Loan Review

(Smart Sampling)

Due Diligence

Quantitative Solutions

Allowance Leader (Comprehensive CECL Solution)

Stress Testing

RESOURCES

The Credit Lifecycle